IRS decisions aren’t always final.

In fact, many taxpayers discover that initial IRS rulings contain errors, incorrect calculations, or oversights. The good news is that the IRS offers several appeal options to challenge these decisions and rectify mistakes before they cost you even more.

Here are the various types of IRS appeals, giving you insight into which is best for your situation and how to initiate the process.

Collection Due Process (CDP) Appeal

A Collection Due Process (CDP) Appeal is a powerful tool for taxpayers facing aggressive collection actions from the IRS such as:

Did you know J David Tax Law can get IRS or State wage garnishments removed within 48 hours? Here’s how

The CDP appeal offers a formal hearing opportunity, which can be conducted as a written hearing, allowing you to present your case, negotiate terms, or dispute the IRS’s actions. It’s an opportunity for taxpayers to pause the collection process and ensure that all actions taken by the IRS are fair and lawful.

When to Use: You should consider filing a CDP appeal when you receive a Notice of Intent to Levy or Notice of Federal Tax Lien from the IRS. These notices give you the right to request a hearing within 30 days of receiving them. This appeal is particularly important if you believe the IRS made a mistake, such as incorrect tax calculations or improperly issued collection actions.

Process:

File Form 12153: Submit within 30 days of receiving a levy or lien notice.

Pause Collection Actions: IRS halts most collection activities while the appeal is reviewed.

Request a Hearing: Present your case before the Office of Appeals.

Propose Solutions: Offer alternatives like an installment agreement or Offer in Compromise.

Receive Outcome: The IRS will issue a decision based on your appeal.

Collection Appeals Program (CAP)

The Collection Appeals Program (CAP) allows taxpayers to dispute IRS collection actions, including liens, levies, and property seizures, before they take place or even after they are enforced. Unlike the traditional appeals process, CAP provides a more streamlined way to resolve collection-related issues without having to wait for the IRS to send a notice of final determination.

CAP covers a wide range of IRS collection actions, such as:

Tax Lien filings

Tax Levy or property seizure

Denial or termination of an installment agreement

IRS rejection of proposed payment plans

To initiate a CAP appeal, taxpayers must file IRS Form 9423 (Collection Appeal Request). One key benefit of the CAP process is that it can stop the collection actions while the appeal is pending, offering immediate protection for your financial assets. However, it’s important to note that CAP decisions cannot be further appealed to the Tax Court, meaning the IRS’s decision is final.

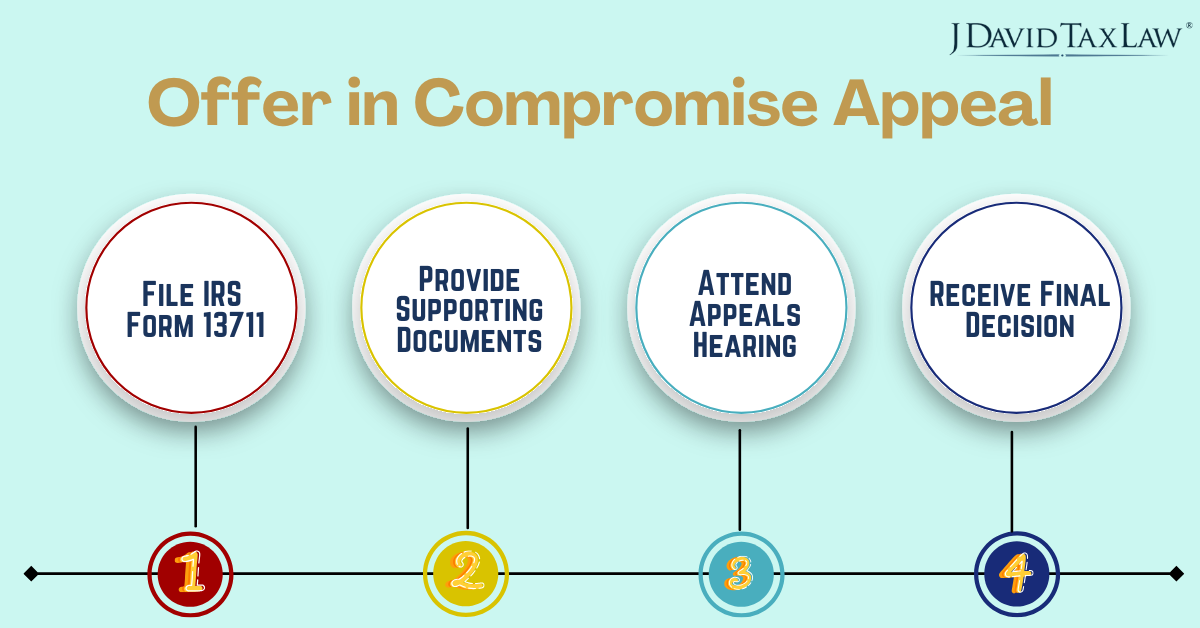

Offer in Compromise Appeal

An Offer in Compromise (OIC) Appeal allows taxpayers to dispute a rejected offer to settle their tax debt for less than the full amount owed. If the IRS believes your offer is too low or doesn’t meet its criteria, you have the right to appeal the decision and provide additional evidence to support your case.

When to Use: You should file an OIC appeal if your initial offer was denied and you believe the IRS didn’t consider all relevant factors, such as your financial situation or ability to pay. This appeal is common when taxpayers feel their offer was reasonable given their circumstances, but the IRS disagrees.

Process:

File IRS Form 13711: Submit the Request for Appeal of Offer in Compromise within 30 days of receiving the rejection using Form 13711.

Provide Supporting Documents: Include any additional financial information to strengthen your case.

Attend Appeals Hearing: Present your case and explain why your offer should be reconsidered.

Receive Final Decision: The IRS will review the appeal and issue a final decision on whether the offer is accepted or modified.

Audit Reconsideration: Appeal Tax Assessment

An audit reconsideration is a process that allows taxpayers to request a reevaluation of their tax assessment after an audit has been completed. This appeal is particularly useful when you have new evidence or documentation that wasn’t available during the initial audit or if you believe the IRS made a mistake in its assessment.

When to Use: You should request an audit reconsideration if you disagree with the results of an IRS audit, especially if you were unable to provide certain documents at the time of the audit, or if you believe the IRS made errors in assessing your taxes. It’s also a good option if you did not respond to the original audit or missed the audit entirely.

Process:

Submit Audit Reconsideration Request: Prepare a written request along with any new supporting documentation (e.g., receipts, financial records) to dispute the original assessment.

Attach Form 4549 or Tax Assessment: Include a copy of the IRS audit report or tax assessment you’re disputing.

IRS Review: The IRS will evaluate the new evidence and reconsider the original audit findings.

Receive Final Determination: The IRS may accept your new evidence, adjust your tax bill, or maintain its original decision.

If you think the process is very complex, our IRS audit attorneys can help you in the audit reconsideration process.

Innocent Spouse Relief Appeal

The innocent spouse relief appeal is designed to protect individuals from being held liable for their spouse’s (or ex-spouse’s) tax debts due to inaccurate or underreported information on joint tax returns. This relief ensures that one spouse is not unfairly burdened by the other’s mistakes or intentional misreporting of income.

When to Use: You should file for innocent spouse relief if you believe your spouse or ex-spouse is solely responsible for errors on your joint tax return, and you were unaware of these issues when the return was filed. Common situations include unreported income, excessive deductions, or fraudulent claims made by your spouse.

Process:

File Form 8857: Submit a Request for Innocent Spouse Relief to the IRS as soon as you discover the tax issue.

Provide Supporting Evidence: Document how you were unaware of the errors, including proof of separation or divorce, financial records, and relevant details about your lack of involvement in the tax filings.

IRS Review: The IRS will review the request, considering factors like the couple’s financial situation, the extent of your knowledge of the tax return, and the fairness of holding you responsible.

Receive Decision: The IRS will issue a final ruling, either granting or denying relief, which can significantly reduce your tax liability.

Did you know that our tax appeal lawyers can offer solutions beyond just appealing? Explore alternatives like Equitable Relief, Separation of Liability Relief, or Injured Spouse Relief to effectively address your tax issues.

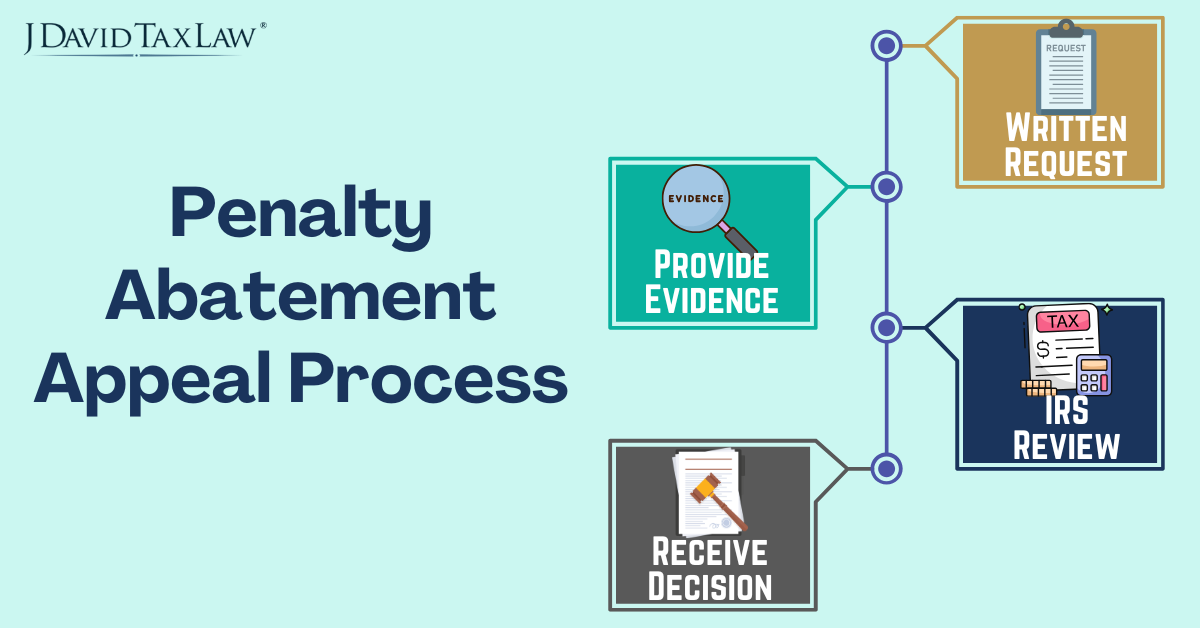

Penalty Abatement Appeal

A penalty abatement appeal allows taxpayers to request the removal or reduction of IRS-imposed penalties, often due to late payments, failure to file, or underpayment of taxes. The IRS recognizes that unforeseen circumstances can prevent timely compliance, and they offer penalty abatement in cases where reasonable cause can be demonstrated.

When to Use: You should consider filing a penalty abatement appeal if you believe you had a legitimate reason for failing to meet IRS deadlines or requirements. Common justifications include medical emergencies, natural disasters, the death of a close family member, or other unavoidable hardships that prevented compliance.

Process:

Submit a Written Request: Send a formal letter or use IRS Form 843, Claim for Refund and Request for Abatement, explaining the reason for your request.

Provide Evidence: Include supporting documentation such as medical records, insurance claims, or legal documents to prove the circumstances that led to the failure.

IRS Review: The IRS will evaluate your case and determine whether your explanation qualifies for reasonable cause.

Receive Decision: You will be informed whether the penalties have been reduced, eliminated, or upheld.

Tax Court Appeal

A tax court appeal is a legal process where taxpayers can challenge IRS decisions by taking their case to the U.S. Tax Court. This option is often a last resort after administrative appeals have been exhausted or if the taxpayer believes that other appeal options won’t lead to a fair resolution. It allows taxpayers to dispute their tax liability before an impartial judge.

When to Use: You should consider a Tax Court appeal if you disagree with the IRS’s final determination after using other appeal processes, or if you receive a Notice of Deficiency (often referred to as a “90-day letter”). This appeal is especially useful for larger or more complex tax disputes, including disputes over tax assessments, penalties, or eligibility for certain tax deductions.

Process:

File a Petition: Submit a formal petition to the U.S. Tax Court within 90 days of receiving the IRS’s Notice of Deficiency.

Prepare Your Case: Gather all relevant documentation, evidence, and legal arguments to present your side of the dispute.

Court Hearing: Present your case before a tax court judge, either representing yourself or with the help of a tax attorney.

Receive Court Ruling: The judge will issue a decision that could either reduce, modify, or uphold the IRS’s assessment.

Our tax appeal attorneys have saved clients thousands of dollars in penalties. Contact us today to see how we can reduce your tax liabilities and penalties effectively!

Wrap Up

Your financial future shouldn’t be dictated by an IRS decision that you disagree with. The appeal options available allow you to defend your position and correct mistakes. From reducing penalties to disputing assessments, knowing how to use these options can significantly impact your financial outcome.

Take advantage of your rights and make sure your financial future is protected by exploring the available appeal processes.

At J. David Tax Law, we’re equipped to act as your power of attorney, representing you directly with the IRS to secure the best possible outcome. Call us today at (888) 342-9436 to start with a team that stands by your side.