If you owe back taxes to the IRS and are unable to pay the full amount upfront, you might be feeling overwhelmed and unsure of what to do next. Fortunately, the IRS payment plan also known as an IRS installment agreement—provides a practical solution for taxpayers to manage their debt. By enrolling in a payment plan, you can settle your tax liability over time through manageable monthly payments, avoiding harsher consequences like wage garnishments or tax liens.

In this blog, we’ll walk you through everything you need to know about how to set up a payment plan with the IRS, the different options available, and why working with a tax attorney may make the process smoother and less stressful.

What Is an IRS Payment Plan?

An IRS payment plan allows taxpayers who owe the IRS more than they can pay immediately to break down their debt into smaller, monthly installments. Instead of facing penalties or more aggressive collection actions, such as IRS levies or wage garnishments, a payment plan for IRS helps ease the financial burden.

There are several types of IRS payment plans, each designed to accommodate different levels of tax debt and financial situations:

Short-Term Payment Plan: Typically for debts under $100,000, to be paid off in 180 days or less.

Long-Term Payment Plan (Installment Agreement): Ideal for larger debts and allows payments over several years.

Streamlined Installment Agreement: For those who owe less than $50,000 and offers a simplified application process.

Partial Payment Installment Agreement (PPIA): This option allows you to pay part of your tax debt over time, with the remaining debt forgiven after the collection period expires.

Why Set Up a Payment Plan with the IRS?

Setting up a payment plan with the IRS can provide several benefits:

Avoid Harsh Penalties: Once you are on a payment plan, you are less likely to face aggressive IRS collection actions such as tax liens or wage garnishments.

Manageable Payments: A payment plan to pay the IRS allows you to break down your tax debt into monthly payments that fit your budget, giving you time to get back on your feet.

Prevent Further Debt Accumulation: While interest and penalties may continue to accrue on the unpaid balance, being on a payment plan for the IRS will prevent additional penalties for failure to pay.

Types of IRS Payment Plans

The IRS offers several types of payment plans, each catering to different debt amounts and financial situations. Here’s a breakdown of the most common options:

1. IRS Short-Term Payment Plan

A short-term payment plan allows you to pay off your tax debt in full within 180 days. This plan is ideal for taxpayers who can resolve their debt in the near future but need a little extra time. With this plan, interest and penalties continue to accrue, but you avoid any long-term commitments.

IRS Payment Plan Eligibility:

Individuals: Must owe less than $100,000 in combined tax, penalties, and interest.

Businesses: Must owe less than $25,000 in combined tax, penalties, and interest.

Application: You can apply for this plan using the online payment plan IRS tool or by submitting IRS Form 9465.

2. IRS Long-Term Payment Plan (Installment Agreement)

The long-term payment plan, also known as the IRS Installment Agreement, allows taxpayers to pay off their debt over a longer period—usually up to 72 months. This plan is suitable for those with larger debts who cannot make a lump-sum payment. You will still accrue IRS penalties and interest, but this plan spreads the payments out to make them more manageable.

Eligibility:

Individuals: Must owe less than $50,000.

Businesses: Must owe less than $25,000.

You can apply through the pay IRS payment plan online tool or by submitting Form 9465.

Need help with IRS Form 9465? Let J. David Tax Law handle the complexities and secure your IRS payment plan today! Call us at (877) 845-2460 for free consultation.

3. IRS Streamlined Installment Agreement

For those who owe less than $50,000, the Streamlined Installment Agreement offers a simplified application process without requiring detailed financial disclosures. You can stretch payments over a period of up to 72 months. As long as you meet the debt threshold and remain compliant with your payments, the IRS will not initiate collection actions.

Benefits:

No need for detailed financial information.

Quick and straightforward approval process.

Application: Submit Form 9465 online or use the IRS Online Payment Agreement tool.

4. Partial Payment Installment Agreement (PPIA)

If you’re unable to pay the full amount of your tax debt, the Partial Payment Installment Agreement (PPIA) might be a viable option. This plan allows you to make monthly payments based on your financial capacity, with the remaining debt being forgiven after the collection period expires (typically 10 years). You will need to submit a detailed financial statement (Form 433-A or 433-B) to qualify for this plan.

Benefits:

Monthly payments are based on your ability to pay.

The IRS may forgive the remaining balance after the collection statute expires.

5. Offer in Compromise (OIC)

An Offer in Compromise allows taxpayers to settle their tax debt for less than the full amount owed. This is typically offered to individuals and businesses that can prove they are unable to pay the full debt either through a lump sum or installment payments. The IRS will evaluate your income, expenses, assets, and overall financial situation before approving an OIC.

Eligibility: You must demonstrate an inability to pay the full tax liability through normal means.

Application: Submit Form 656 along with Form 433-A (for individuals) or 433-B (for businesses).

Struggling with tax debt and traditional solutions aren’t working? We’ve helped our client settle $11K for just $200—visit https://www.jdavidtaxlaw.com/tax-learning-center/ & find out how we can help today!

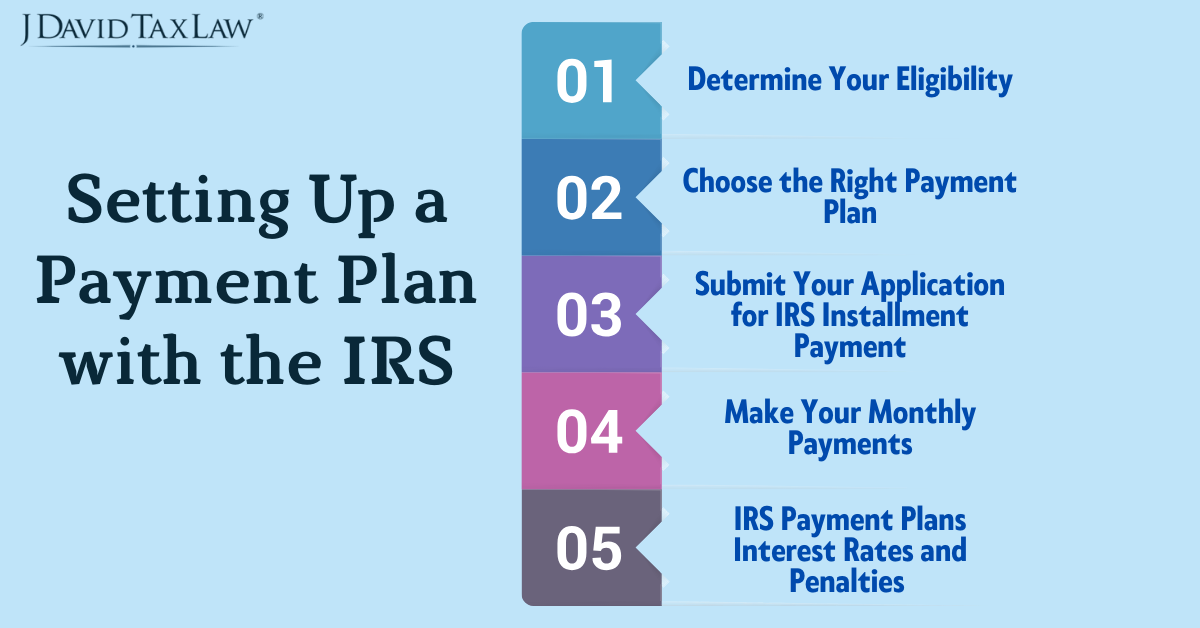

Setting Up a Payment Plan with the IRS

Setting up an IRS payment plan may seem daunting, but by following a few steps, you can make the process smoother. Here’s how you can apply:

1. Determine Your Eligibility

To begin, determine whether you qualify for the type of IRS payment plan that suits your situation. Generally, you may qualify for an IRS short-term payment plan if you owe less than $100,000 in combined tax, penalties, and interest. If you owe more than $50,000, an IRS long-term payment plan may be necessary.

2. Choose the Right Payment Plan

The IRS offers different payment plan options depending on how much you owe and how long you need to repay your debt:

IRS Short-Term Payment Plan: If you can pay your debt in full within 180 days, this is the simplest option. It does not require extensive financial documentation, and you can apply online via the online payment plan IRS tool.

IRS Long-Term Payment Plan (Installment Agreement): If your tax debt exceeds $50,000 or you need more than 180 days to repay, you can apply for a long-term IRS payment plan. This requires submitting IRS Form 9465, either by mail or through the IRS payments online plan payment tool.

Streamlined Installment Agreement: This plan is perfect for taxpayers who owe less than $50,000 and need to repay their debt over several years. The application process is more straightforward because it doesn’t require detailed financial disclosures.

Partial Payment Installment Agreement (PPIA): If you are unable to pay your debt in full and your financial situation qualifies you for this option, you can submit Form 433-F to demonstrate your financial hardship and set up partial monthly payments.

3. Submit Your Application for IRS Installment Payment

The easiest way to set up a payment plan with the IRS is through their online portal. Here’s how you can do it:

Apply Online: You can apply for both short-term and long-term payment plans through the online payment plan IRS tool. Simply go to the IRS website, select “Payment Plans,” and follow the prompts to enter your financial information and choose your plan.

Apply by Mail: For more complex situations, especially if you’re applying for a Partial Payment Installment Agreement, you’ll need to submit IRS Form 9465 (Installment Agreement Request) along with any required financial disclosures.

Work with a Tax Attorney: While you can certainly apply on your own, hiring a professional tax attorney from J. David Tax Law can significantly increase your chances of success. An experienced tax attorney can help you negotiate the most favorable terms and ensure that your application is accurate and complete.

4. Make Your Monthly Payments

Once your IRS payment plan is approved, it’s important to stay current with your monthly payments. Missing a payment could result in additional penalties, interest, or even termination of your payment plan.

You can make payments through the pay IRS payment plan online tool or by setting up a direct debit from your bank account to avoid missing any payments.

5. IRS Payment Plans Interest Rates and Penalties

When you set up an IRS payment plan, it’s important to understand that interest and penalties will continue to accrue until your tax debt is fully paid off. The IRS charges interest on unpaid taxes, which is compounded daily, along with late payment penalties. The IRS charges a penalty of 0.5% of the unpaid tax for each month the debt remains unpaid, up to a maximum of 25%. Interest is also charged on the balance at the current federal short-term rate plus 3%. For long-term payment plans, this can significantly increase the total amount you owe over time, making it important to stay compliant with your payments to avoid additional costs.

Maintaining Your IRS Payment Plan

After setting up an IRS payment plan, it’s important to stay compliant. This means:

Filing all future tax returns on time.

Making your monthly payments consistently.

Updating the IRS if your financial situation changes.

Failure to meet these requirements could result in penalties, interest, or even the termination of your payment plan for IRS. To avoid any issues, it’s important to regularly monitor your plan and ensure you’re staying on track.

How to Modify or Cancel Your IRS Payment Plan

If your financial situation changes, you may need to modify your IRS payment plan to add new tax debts or adjust your monthly payment. To request changes, you can contact the IRS or use the IRS Online Payment Agreement tool to modify your plan. If you wish to cancel your IRS payment plan, you will need to pay off the remaining balance in full. In case of missed payments, you may reinstate your IRS repayment plan to avoid collection actions. Failure to make modifications or cancelations properly can result in penalties, so working with a tax attorney can ensure the process is handled correctly.

Why Choose a Professional Tax Debt Attorney for Setting Up a Payment Plan?

IRS payment plan process can be complex and time-consuming. Working with an experienced tax debt attorney from J. David Tax Law can make the process easier and improve your chances of getting approved for the best possible terms.

With four decades of collective experience, Our team specializes in helping individuals and businesses across all 50 states set up IRS payment plans, including online payment plan IRS applications, handling all necessary paperwork, and negotiating with the IRS to secure favorable terms. Plus, we offer free consultations to get you started on the path to financial relief. Don’t risk making costly mistakes let our professional tax debt attorneys help you through every step of the process.

Final Thoughts

Setting up a payment plan with the IRS is a smart option for taxpayers struggling with tax debt. By following the steps outlined above, you can take control of your financial situation and avoid harsher IRS collection actions. Remember, the key to success is choosing the right plan for your situation and ensuring your application is accurate and complete.