Owing taxes to the IRS is already stressful, but what makes it worse is the additional cost of penalties and interest. When you fail to pay your tax balance on time, the IRS charges penalties, and on top of that, it adds interest that keeps growing until the balance is fully paid.

Understanding how the IRS calculates interest on tax penalties is crucial to minimize your overall tax debt. This guide will break down how the IRS calculates interest on tax penalties, what factors influence the amount owed, and how you can take action to avoid excessive costs.

How the IRS Calculates Interest on Tax Penalties

Remember that the IRS not only imposes penalties but also charges interest on those penalties when a taxpayer fails to pay taxes. They follow a standardized formula for calculating interest on tax penalties. The key components of this include:

Interest Starts Accruing Immediately

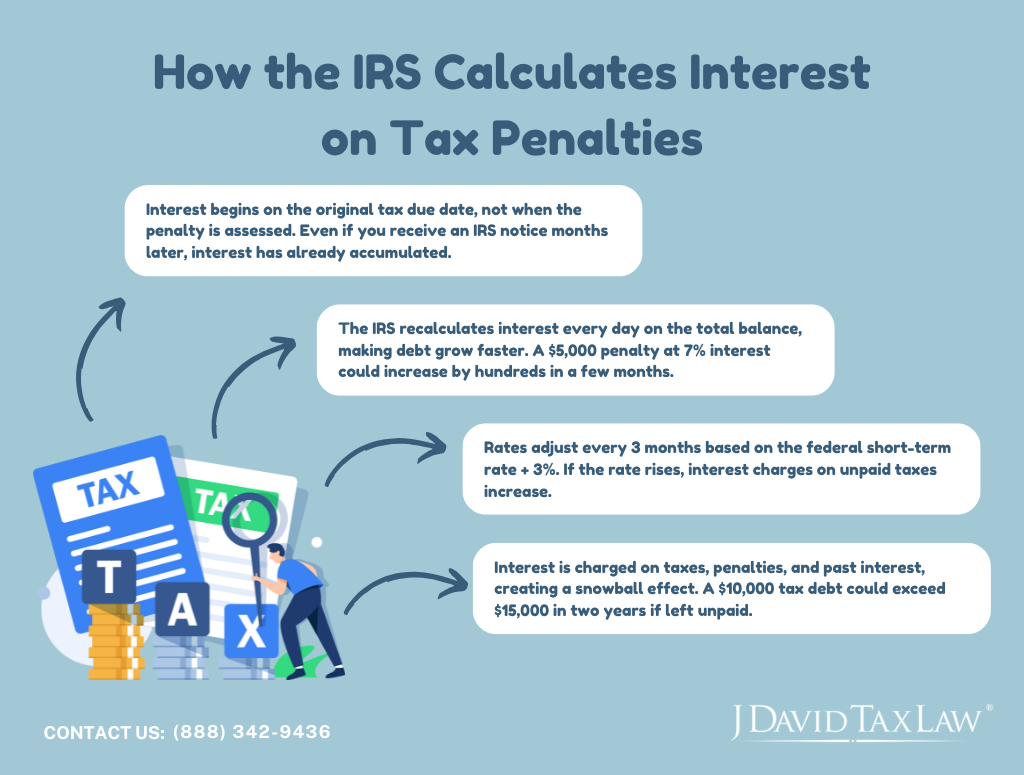

One of the most important things to understand is that interest on penalties doesn’t wait to start accumulating. It begins accruing from the original due date of the tax return or payment, not from the date the penalty was issued.

For example:

If your tax return was due on April 15, 2024, but you didn’t file and pay until October 15, 2024, the IRS may assess a failure-to-file penalty and a failure-to-pay penalty in October. However, the interest on these penalties will retroactively start from April 15, 2024.

This means that by the time you receive an IRS notice about your penalties, the amount you owe is already higher due to months of accumulated interest.

Interest is Compounded Daily

Unlike simple interest, which is calculated only on the original penalty amount, the IRS applies daily compounding interest. This means that the interest is recalculated every day based on the total balance owed, including any unpaid taxes, penalties, and previously accrued interest.

How daily compounding works:

Let’s say you have a $5,000 tax penalty, and the IRS charges a 7% annual interest rate. Here’s how daily compounding increases your debt:

The daily interest rate is calculated as 7% ÷ 365 days = 0.0192% per day

On Day 1, your interest is $5,000 × 0.0192% = $0.96

On Day 2, your new balance is $5,000.96, and interest is recalculated on this amount.

By Day 30, you owe $5,147.04—that’s an extra $147.04 in just one month!

Over a year, you could owe hundreds or even thousands of dollars more depending on the balance and interest rate.

Because of this compounding effect, the longer your penalties remain unpaid, the faster your balance grows. Many taxpayers underestimate just how quickly IRS interest can turn a manageable penalty into a significant financial burden.

IRS Interest Rates Are Set Quarterly

The IRS updates its interest rates every three months based on the federal short-term rate plus 3% (for individuals). The rate fluctuates depending on economic conditions, but once it applies to your debt, it continues accruing until fully paid.

Here’s how this works:

The IRS bases its interest rates on the federal short-term rate, which is determined by the U.S. Treasury.

The standard formula for individuals is: IRS Interest Rate = Federal Short-Term Rate + 3%

If the federal short-term rate is 4%, then the IRS interest rate for that quarter would be 4% + 3% = 7%.

Interest Applies to the Entire Unpaid Balance

Interest is charged on penalties and on the total unpaid balance, which includes taxes, penalties, and previously accrued interest. This creates a snowball effect: the longer you wait, the more you owe.

Let’s say a taxpayer owes $10,000 in unpaid taxes and incurs the following penalties:

Failure-to-file penalty: $2,500

Failure-to-pay penalty: $500

Total balance before interest: $13,000

If the IRS interest rate is 7% annually, the daily compounding will increase the debt significantly:

After 6 months: ~$13,500

After 1 year: ~$14,000

After 2 years: ~$15,000+

This taxpayer could end up paying thousands more than the original tax bill by delaying payment.

Factors That Determine IRS Interest on Tax Penalties

The amount of interest the IRS charges on tax penalties is influenced by a few key factors, all of which affect how quickly your balance grows. While interest is always compounded daily, the total amount you owe depends on the following.

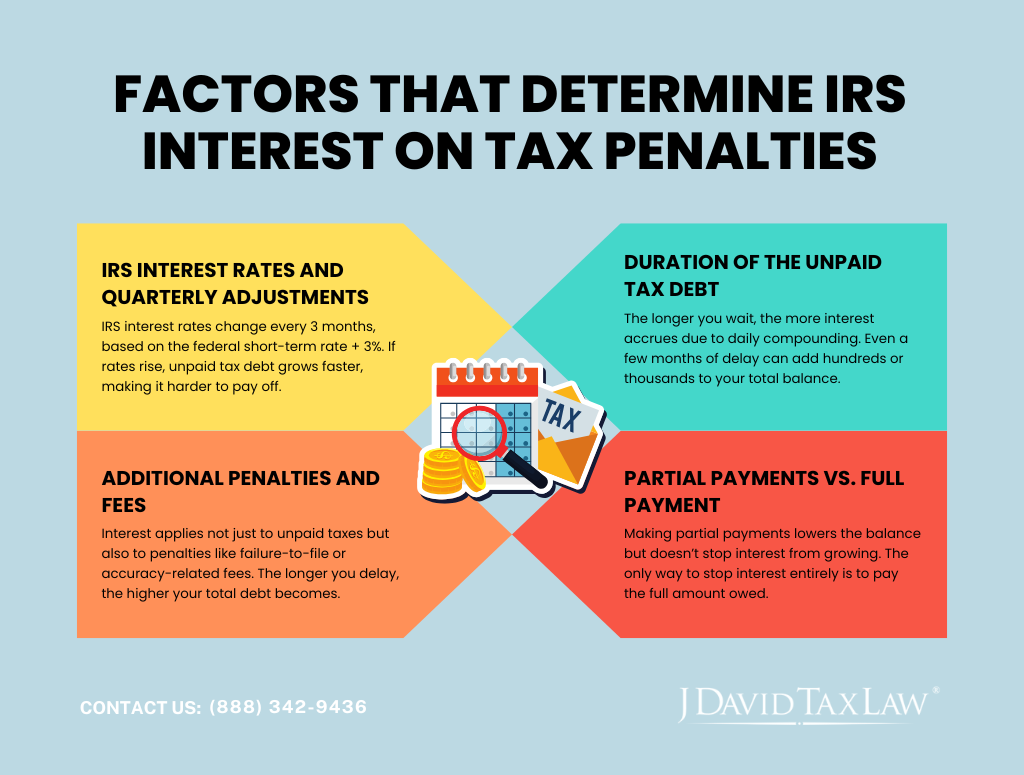

IRS Interest Rates and Quarterly Adjustments

IRS interest rates are not fixed—they change every quarter based on the federal short-term rate plus 3% for individuals. This means that interest rates fluctuate with market conditions, and taxpayers with long-standing unpaid balances may find their interest costs increasing over time.

For example, if the federal short-term rate rises from 4% to 5%, the IRS interest rate also increases, causing tax debt to grow even faster. These quarterly adjustments make it difficult to predict exactly how much interest will accrue, especially if penalties remain unpaid for an extended period.

Duration of the Unpaid Tax Debt

The longer a tax penalty remains unpaid, the more interest accumulates. Since the IRS compounds interest daily, even short delays in payment can significantly increase the total balance. Interest does not stop accruing until the full amount is paid in full. Many taxpayers are unaware that waiting just a few months to resolve their balance can result in owing hundreds or even thousands more than their original tax bill.

Additional Penalties and Fees

Interest is not just applied to the original unpaid tax amount. It also accrues on penalties such as:

Failure-to-file

Failure-to-pay

Accuracy-related penalties

If a taxpayer delays payment for an extended period, they may face additional penalties that increase the principal balance, causing even more interest to accrue. This snowball effect makes it essential to resolve tax debts quickly before they become overwhelming.

Partial Payments vs. Full Payment

While making partial payments can help reduce the total balance, it does not stop interest from accruing. The IRS continues charging interest on any remaining unpaid amount until the full debt is satisfied. Taxpayers who enter into installment agreements or payment plans should be aware that interest will continue to accumulate on the outstanding balance, potentially making their repayment more expensive in the long run. The only way to completely stop IRS interest from growing is to pay off the entire balance as soon as possible.

Can You Reduce or Eliminate IRS Interest on Tax Penalties?

While IRS penalties can sometimes be reduced or waived, interest is much harder to eliminate. The IRS does not typically reduce or forgive interest charges unless the associated penalties are removed. However, taxpayers do have options to reduce the total amount owed and limit how much interest accumulates.

Here are some of the most common tax penalty relief options:

First-Time Penalty Abatement (FTA)

If a taxpayer has a history of compliance and has not faced penalties in the past three years, they may qualify for First-Time Penalty Abatement (FTA). Since interest is charged on penalties, removing the penalty also eliminates the associated interest. However, FTA does not apply to interest itself—only the penalties that caused it.

Reasonable Cause Relief

Taxpayers who can prove they had a valid reason for failing to file or pay on time may qualify for Reasonable Cause Relief. Examples of reasonable cause include:

Serious illness or injury

Natural disasters

Unavoidable absence (such as military deployment)

Incorrect tax advice from a professional

If the IRS grants relief, the penalties are removed, and the interest charged on those penalties is also eliminated. However, interest on the original unpaid tax balance remains.

Payment Plans and Settlements

Even if penalties and interest cannot be waived, setting up a payment plan can help prevent further increases in IRS debt. The IRS offers several payment options, including:

Installment Agreements – Allow taxpayers to make monthly payments on their debt, though interest continues to accrue.

Offer in Compromise (OIC) – In some cases, the IRS may accept a lower amount than what is owed to reduce both penalties and interest.

Currently Not Collectible (CNC) Status – If a taxpayer can prove financial hardship, the IRS may pause collection efforts, though interest continues to accumulate.

Paying Off the Balance as Soon as Possible

The most effective way to stop IRS interest from growing is to pay off the balance in full. Since interest compounds daily, even minor delays can result in a higher total debt. Using savings, taking out a loan, or negotiating a settlement can sometimes be more cost-effective than allowing interest to keep increasing.

Conclusion

IRS interest on tax penalties doesn’t wait, and neither should you. With daily compounding, what seems like a small penalty today can quickly snowball into an unmanageable debt. The best way to stop interest from growing is to act fast, whether paying off the balance, applying for penalty relief, or setting up a structured repayment plan.

J. David Tax Law can help taxpayers take immediate action to prevent unnecessary interest and penalties. If you’re facing growing tax debt, don’t wait until it’s too late.

Contact us today and let our team of tax debt attorneys negotiate the best possible resolution on your behalf.