Facing rejection for your Offer in Compromise (OIC) can be frustrating, especially when you are hoping for a lifeline to your tax troubles. But don’t worry—being declined isn’t the end of the road. Many taxpayers experience this setback, and the good news is there are still several paths forward.

Here are the steps you can take after a denial to get back on track and find the right solution for your tax debt.

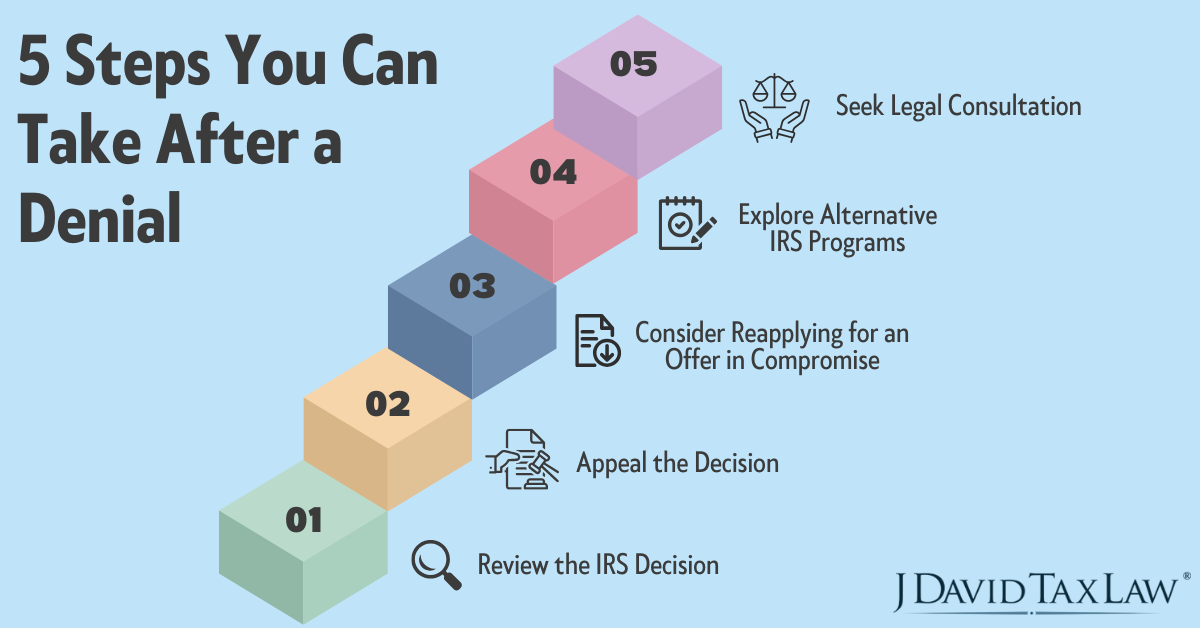

Step 1: Review the IRS Decision

Before taking your next step, it’s crucial to understand why the IRS declined your Offer in Compromise. The rejection letter will outline specific reasons for denial such as:

Missing information

Incomplete financial documentation

IRS’s belief that you can afford to pay more than you offered.

Carefully review these details to pinpoint what went wrong in your initial application. Once you’ve identified the reason for the rejection, you’ll be better equipped to adjust your approach. Understanding the IRS’s logic behind the denial will help you avoid making the same mistake if you decide to appeal or reapply.

Step 2: Appeal the Decision

If you believe the IRS’s decision to reject your Offer in Compromise was unjust, you have the right to appeal.

Filing an appeal gives you the chance to present your case again, especially if you think the IRS overlooked crucial information or if you can provide additional evidence to support your offer. You can start this process by submitting IRS Form 13711 (Request for Appeal of Offer in Compromise) within 30 days of receiving the denial notice.

When preparing your appeal, it’s essential to address the reasons for the rejection, offering clear explanations or updated documentation to strengthen your case. Working with a J. David Tax Law attorney during this process can ensure you meet all requirements and maximize your chances of success.

Step 3: Consider Reapplying for an Offer in Compromise

If an appeal isn’t the right path, or if your financial situation has changed since your initial application, reapplying for an Offer in Compromise may be a viable option. Before reapplying, take the time to address the issues that led to your rejection. This could involve the following:

Providing more thorough financial documentation

Updating your income and expenses

Adjusting the amount you’re offering to pay

Reapplying can often lead to a more favorable outcome if you can demonstrate significant changes in your financial circumstances or better align your offer with the IRS’s expectations. However, it’s crucial to carefully review the IRS guidelines to ensure your new application is stronger than the first.

Step 4: Explore Alternative IRS Programs

If reapplying for an Offer in Compromise doesn’t seem like the best route, it’s important to explore other IRS programs that can still provide relief from your tax debt. There are several alternatives to consider, depending on your financial situation:

Installment Agreement: If you can’t pay the full amount of your tax debt upfront, an installment agreement allows you to make manageable monthly payments over time. This option is ideal for taxpayers who can afford smaller, consistent payments.

Currently Not Collectible Status (CNC): If you’re experiencing financial hardship and can’t pay anything toward your tax debt, you may qualify for Currently Not Collectible status. This temporarily halts collection actions like wage garnishments and bank levies until your financial situation improves.

Penalty Abatement: If your tax debt has accumulated penalties due to late filing or payment, you may qualify for penalty abatement. This program can reduce or remove penalties, lightening the burden of your overall debt.

Innocent Spouse Relief: Innocent Spouse Relief provides an alternative to an Offer in Compromise by relieving taxpayers from joint liability for taxes due to errors or omissions made by their spouse or former spouse. This relief ensures that individuals aren’t held responsible for underreported income or improper deductions they had no knowledge of.

Step 5: Seek Legal Consultation

When your Offer of Compromise is rejected, navigating the next steps on your own can be overwhelming. This is where seeking the expertise of a tax attorney can make all the difference.

At J. David Tax Law, we understand how frustrating it can be when your Offer in Compromise is declined. That’s why we’re here to help you navigate the complex next steps. Our experienced tax attorneys will carefully review the IRS’s decision, assess your financial situation, and guide you toward the best strategy.

Whether it’s appealing the decision, reapplying, or exploring alternative tax relief options like installment agreements or penalty abatements, we are here to help.

Wrap Up

A rejection of your Offer in Compromise might feel like a setback, but it’s far from the end toward resolving your tax debt. By carefully reviewing the IRS’s decision, appealing if necessary, or reapplying with stronger documentation, you can still find relief.

At J. David Tax Law, we specialize in helping taxpayers like you overcome these challenges. With the right strategy and legal support, you can turn this temporary obstacle into a manageable solution for your tax issues. Reach out to us and let us guide you every step of the way, ensuring that your next move is a successful one.