If you’re struggling with tax debt and feel overwhelmed by the amount you owe, there may be a solution that allows you to pay less than the full amount.

An Offer in Compromise (OIC) is a program offered by the IRS that gives qualifying taxpayers the opportunity to settle their tax liabilities for less than they actually owe. It’s a legitimate way to resolve your tax debt, especially when full payment would create a significant financial burden.

While not everyone qualifies, understanding the process and criteria for an OIC can provide a lifeline for taxpayers facing serious financial challenges.

What is an Offer in Compromise?

An Offer in Compromise (OIC) is an IRS program designed to help taxpayers settle their tax debt for less than the full amount owed. It’s a solution for individuals and businesses facing significant financial difficulties, where paying the full debt would be unrealistic or create an undue financial burden. By offering a lower amount, taxpayers can negotiate a fresh start with the IRS, potentially wiping out a portion of their debt.

The Offer in Compromise Process

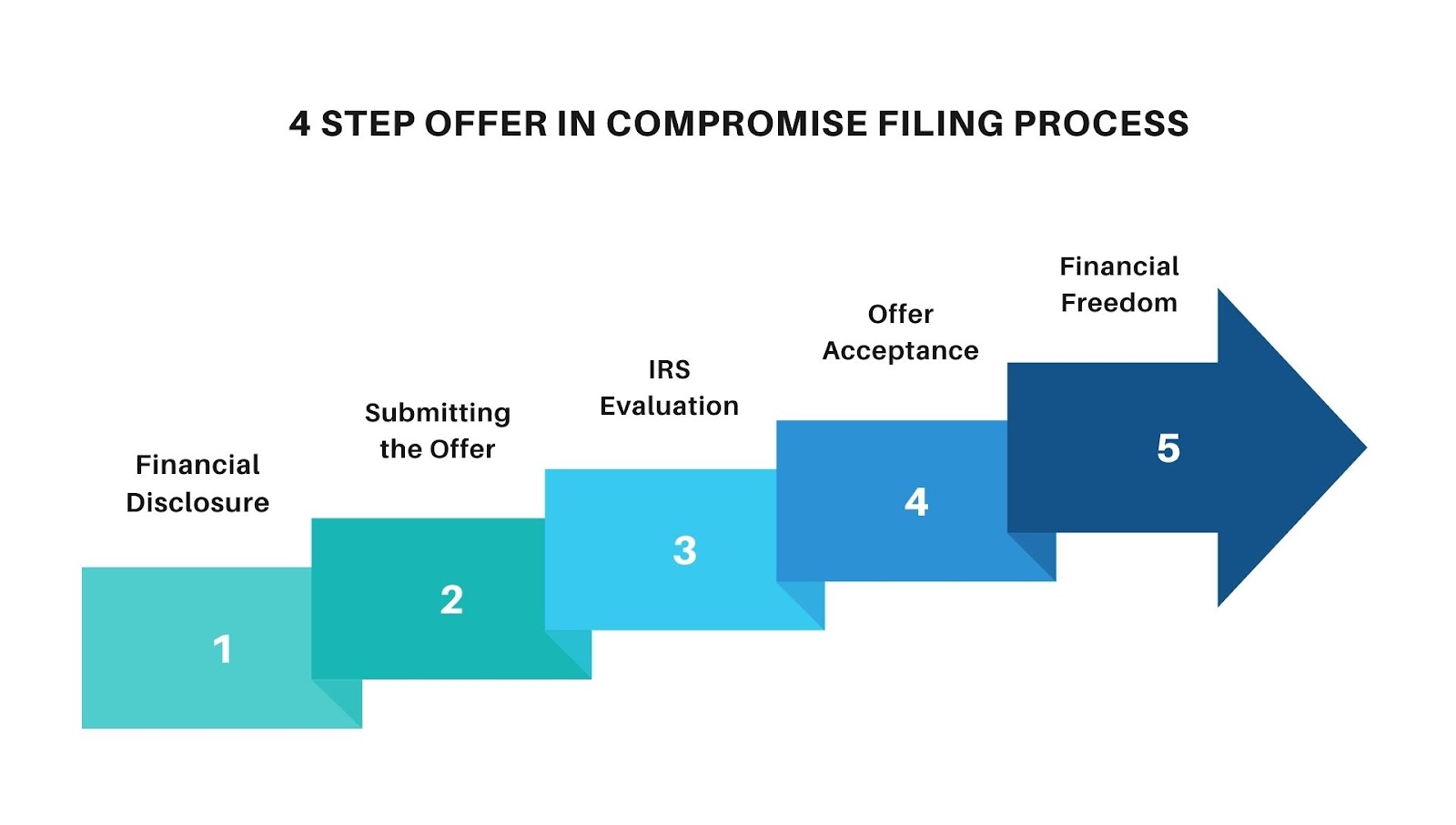

The Offer in Compromise process involves several key steps that must be followed to successfully submit your application to the IRS. While it may seem straightforward, the process requires detailed financial disclosures and a strategic approach to increase your chances of acceptance.

Here’s a breakdown of how it works:

Step 1: Financial Disclosure

The first step involves gathering and submitting detailed financial information. This includes filling out Form 433-A (for individuals) or Form 433-B (for businesses). These forms require you to disclose your income, expenses, assets, and liabilities. It’s crucial to be accurate and thorough in this stage since the IRS uses this data to assess your ability to pay.

Step 2: Submitting the Offer

Once your financial information is in order, you’ll submit Form 656, the official Offer in Compromise application. This form indicates the amount you’re offering to settle your tax debt.

Keep in mind that you’ll also need to make an initial payment with your offer. This can be either a lump sum or set up as part of a payment plan.

Step 3: IRS Evaluation

After your offer is submitted, the IRS will begin evaluating your case. This process can take several months and may involve the IRS requesting additional documentation or clarification.

During this period, the IRS will consider factors such as your reasonable collection potential (RCP). RCP is an estimate of the amount they believe they can collect from you based on your financial disclosures.

Step 4: Offer Acceptance or Rejection

The IRS will either accept or reject your offer based on their evaluation. If accepted, you will pay the agreed-upon amount, and the rest of your tax debt will be forgiven. If rejected, you have the right to appeal the decision.

In either case, maintaining compliance with all tax filings and payments during the process is essential to avoid disqualification.

Conclusion

An offer in compromise can be a valuable tool for taxpayers struggling with overwhelming tax debt, providing a way to settle for less than what’s owed. While not everyone qualifies, understanding the eligibility criteria and following the correct process can increase your chances of success.

By working with a knowledgeable tax attorney, you can navigate the complexities of the OIC application, ensuring accurate financial disclosures and maximizing your chances of a favorable outcome. With the right strategy, an OIC could offer you the fresh financial start you need, relieving the burden of unpaid taxes.

If you’re considering an offer in compromise and need expert assistance, contact our experienced tax attorneys today. J. David Tax Law can help you assess your eligibility and guide you through the process, giving you the best chance at achieving financial relief.