Tax refund garnishment allows state and federal agencies to take your refund for unpaid debt. With the right steps, it’s preventable. Call (888) 342-9436.

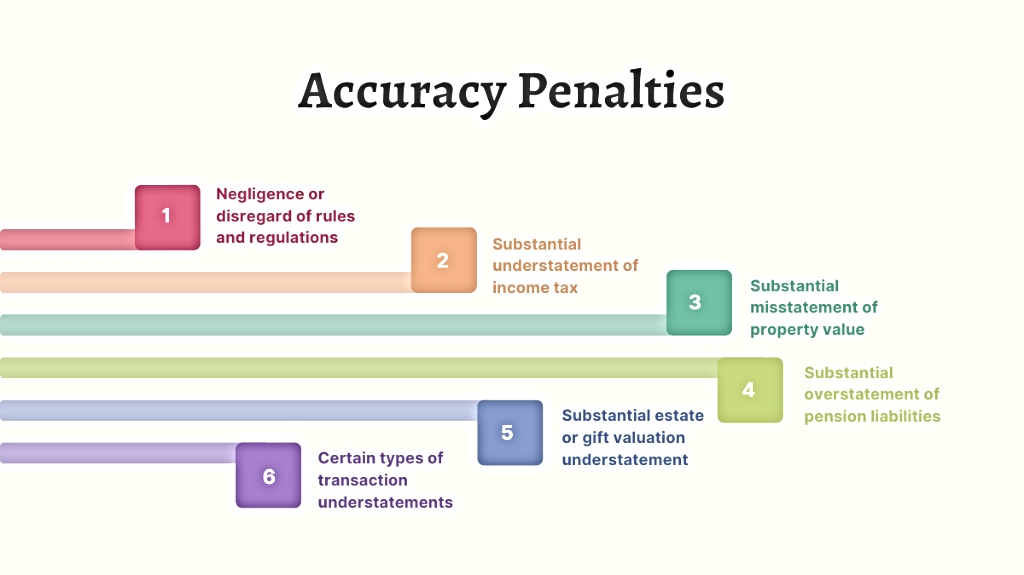

Under the Internal Revenue Code (IRC) § 6662, accuracy-related penalties are imposed when tax returns contain errors. These penalties are typically 20% but can increase to 40% for more severe infractions, such as gross valuation misstatements of property. Common reasons for these penalties include negligence, substantial understatement of income, or a significant misstatement of property value.

Several key factors are taken into account when determining the imposition of accuracy-related penalties:

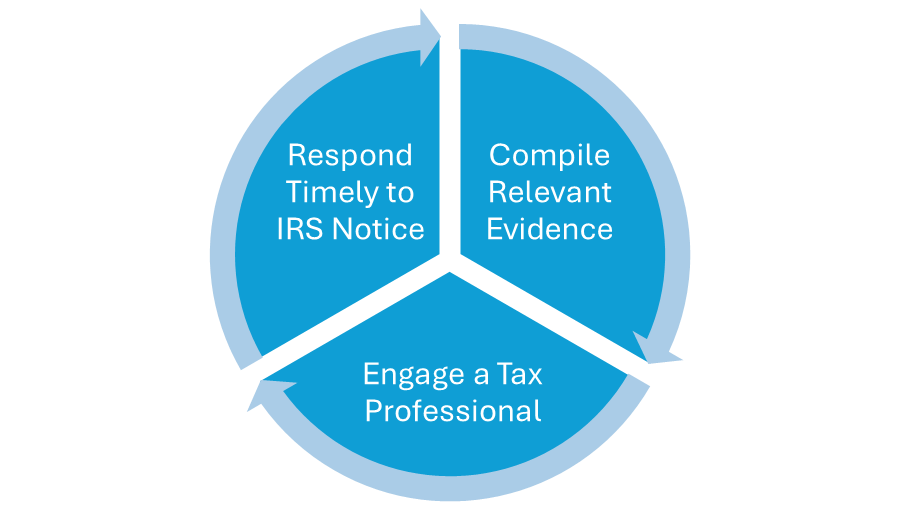

Taxpayers can challenge accuracy-related penalties if they believe there’s a valid reason for abatement, such as reasonable cause and good faith. To dispute these penalties, taxpayers should provide detailed documentation and explanations to the IRS. This might include records that demonstrate due diligence in tax calculations or clarify misunderstandings about reported values.

For more severe penalties like those for gross valuation misstatements, taxpayers face a higher burden of proof. They must convincingly demonstrate that their valuations were reasonable and made in good faith. Engaging a tax professional can be beneficial, as they can provide expert advice on navigating the complexities of the IRS’s standards and help in building a strong case for abatement.

If you have been assessed any penalties by the IRS, it’s crucial to present a strong case. Our team at J David Tax Law is equipped to help you demonstrate that your valuations were reasonable.

Tax fraud is defined by the IRS as a willful and intentional effort to evade tax regulations or defraud the government. The Internal Revenue Service (IRS) takes tax fraud very seriously, imposing strict penalties on those who intentionally deceive or attempt to evade tax laws.

The consequences for committing tax fraud are severe. Under Section 6663 of the Internal Revenue Code (IRC), individuals or entities found guilty of fraud face a civil fraud penalty. This penalty is substantial—75% of the tax underpayment attributable to the fraud. These penalties serve as a powerful deterrent, emphasizing the seriousness of such offenses and underscoring the importance of adherence to tax laws.

Though facing fraud penalties from the IRS can be intimidating, taxpayers have avenues to defend themselves by demonstrating “reasonable cause” for their actions.

If you’re dealing with IRS penalties and feel overwhelmed by the complexities of tax regulations, don’t face it alone. Contact us today at (888) 342-9436 for a free consultation and take the first step towards resolving your IRS penalties with confidence.

Tax refund garnishment allows state and federal agencies to take your refund for unpaid debt. With the right steps, it’s preventable. Call (888) 342-9436.

Read the latest news about the 2024 IRS data and key insights from J. David Tax Law. Call (888) 342-9436.today for a free consultation.

Facing an IRS collection notice? Learn what it means, how to protect your assets, and how we can stop wage garnishments and levies. Call (888) 342-9436