Last updated on November 16th, 2025 at 06:22 pm

If you’ve received a notice from the IRS about unpaid taxes, wage garnishment could be the next step they take to collect the debt. Without quick action, the IRS can begin taking money directly from your paycheck, leaving you scrambling to make ends meet.

IRS wage garnishment is one of the most powerful tools the government has for collecting unpaid taxes, and it doesn’t require a court order. Once the IRS begins the process, your employer will be legally required to withhold a portion of your paycheck and send it directly to the IRS.

Read on to learn how the IRS uses wage garnishment to recover taxes and your options to prevent or resolve the garnishment before it escalates.

Basics of Wage Garnishment

Wage garnishment refers to a legal process where a portion of an individual’s earnings is withheld by their employer to pay off a debt. This can include unpaid taxes, child support, student loans, or consumer debts. The employer forwards the deducted amount directly to the creditor or government agency as mandated by a court order or federal regulations.

How Does Wage Garnishment Work?

Once a creditor or government agency initiates garnishment, they will notify the individual of the debt obligation. The employer, known as the garnishee, will receive a garnishment notice requiring them to withhold a specific percentage of the employee’s wages. These deductions continue each pay period until the full debt, including fees and interest, is satisfied or a legal agreement halts the garnishment.

Learn more about IRS wage garnishment by reading this free resource from our tax debt attorneys.

Legal Basis: Consumer Credit Protection Act and Federal Minimum Wage

The Consumer Credit Protection Act (CCPA) protects employees by setting limits on how much can be garnished from their wages. It ensures that the garnished amount does not exceed a certain percentage, preventing undue financial hardship.

In addition, under federal law, wage garnishment must not reduce the employee’s earnings below the federal minimum wage. If an individual’s wages are close to the minimum wage threshold, the garnished amount may be limited or even deferred. This ensures the individual retains enough income for basic living expenses.

Types of Wage Garnishment

IRS Garnishments

The IRS can impose a wage levy if taxpayers fail to resolve unpaid federal taxes. Unlike other garnishments, the IRS can legally take a more significant portion of wages, leaving the individual with only a minimum amount to cover essential living expenses. IRS wage garnishments continue until the debt is fully paid or an alternative resolution, like an installment agreement or offer in compromise, is established.

Administrative Wage Garnishment

An administrative wage garnishment (AWG) allows federal agencies, such as the Department of Education, to garnish wages without going through court proceedings. This type of garnishment is most commonly used for student loan defaults or other government-related debts. Typically, agencies are limited to garnishing up to 15% of disposable earnings, but exceptions may apply depending on individual circumstances.

Common Reasons for Wage Garnishment

Tax Debts

The IRS and state tax agencies can garnish wages to recover unpaid taxes. IRS garnishments differ from other types because they bypass courts and may take more aggressive deductions, significantly impacting the taxpayer’s take-home pay.

Process Overview of IRS Wage Garnishment

Notice of Garnishment

Before garnishing wages, the IRS sends several notices to the taxpayer, giving them a chance to resolve the debt. The process typically starts with a Notice of Intent to Levy and Notice of Your Right to a Hearing (also called a Final Notice).

The taxpayer has 30 days from the date of the final notice to respond. This is either by paying the debt, setting up an installment agreement, or filing an appeal. Failure to act within this timeframe allows the IRS to initiate garnishment.

Who Can Garnish Wages and Under What Circumstances?

While the IRS has the authority to garnish wages without a court order, certain conditions must be met:

-

The taxpayer must have an outstanding federal tax debt.

-

Multiple notices must be sent, including a Final Notice of Intent to Levy.

-

The taxpayer must not have responded within the designated time or made arrangements for repayment.

In addition to the IRS, other entities such as state tax agencies, family courts, and federal loan agencies can also garnish wages under specific legal conditions.

Role of the Garnishee in Wage Garnishment

The garnishee is the employer responsible for withholding the garnished amount from the taxpayer's paycheck and sending it to the appropriate government agency or creditor. Employers must comply with the garnishment notice to avoid penalties, but they are also protected by law from terminating employees because of a single wage garnishment.

Employers are required to follow the rules outlined in the garnishment order, such as calculating the correct deduction and ensuring compliance with federal wage limits. They may also notify the employee of the garnishment, but by the time it reaches the garnishee, there are limited options to halt the process unless the debt is resolved or legal intervention occurs.

Implications and Employee Rights

Wage garnishment can significantly reduce an employee’s paycheck, affecting their ability to meet financial obligations like rent, utilities, and other bills. IRS garnishments are often more aggressive, leaving the employee with only the amount allowed for basic subsistence.

For employees living paycheck to paycheck, even minor garnishments can disrupt their financial stability, leading to challenges such as:

-

Missed bill payments

-

Accumulation of late fees or penalties

-

Potential damage to credit scores

With that, there are rights under the Consumer Credit Protection Act (CCPA) that protect employees against wage garnishments. Here’s how CCPA works:

-

Limiting the garnishment amount: The law ensures that wage garnishments do not exceed 25% of disposable income or the amount by which disposable earnings exceed 30 times the federal minimum wage—whichever is lower.

-

Prohibiting employer retaliation: Employers are not allowed to fire or penalize employees for having a single wage garnishment. However, multiple garnishments from different sources may affect employment decisions.

Employees can also identify the source of wage garnishment by reviewing their paycheck stubs, which typically list the garnishing party and the deducted amount. In cases of IRS garnishment, the IRS will have sent notices, including the Notice of Intent to Levy.

How to Stop a Wage Garnishment Immediately

Stopping wage garnishment requires immediate action. Some common ways include paying off the debt in full, negotiating a payment plan, or filing for bankruptcy to halt garnishments temporarily.

In the case of IRS garnishments, setting up an installment agreement or applying for currently non-collectible status or an offer in compromise can also provide quick relief.

If you are not confident in going around these options, engage a wage garnishment lawyer from J. David Tax Law may be for you. They can provide you with valuable legal support to address garnishment issues. Here’s how:

-

Identify errors in the garnishment order and challenge unlawful deductions.

-

Negotiate with creditors or the IRS to reduce the garnishment amount.

-

Assist with filing bankruptcy if necessary to halt garnishment.

-

Represent clients in hearings to modify or stop garnishments.

Having professional legal assistance ensures that employees understand their rights and options, preventing unnecessary financial losses. If you want to learn more about your options to stop a wage garnishment, checking out our blog “IRS Taking Your Pay? How to Halt Wage Garnishment Immediately” can help.

Garnishment Relief Options (Payment Plans, Settlements)

Installment Agreements

This option allows individuals to set up a payment plan with the IRS, spreading their tax debt over manageable monthly installments.

Once the agreement is approved, the IRS will pause wage garnishments as long as payments are made on time. This is ideal for those who cannot pay the full amount upfront but want to avoid additional collection actions.

Offer in Compromise

The IRS offers this program for taxpayers who can demonstrate that paying the full debt would cause financial hardship.

If approved, the taxpayer can settle their debt for a fraction of the original amount owed. Wage garnishments will be lifted once the offer is accepted and payments begin, providing significant relief for those under financial strain.

Hardship Exemptions

Courts and government agencies may grant hardship exemptions if the garnishment leaves the individual unable to meet essential living expenses, such as rent, utilities, or food. When approved, garnishments are suspended or reduced temporarily, giving the individual time to improve their financial situation or find an alternative debt resolution.

Debt Settlements

In cases involving non-tax debts, creditors may agree to negotiate a reduced payoff amount in exchange for stopping the garnishment. Debt settlements are especially useful for individuals with limited financial resources, as they can result in significant reductions in the total amount owed. However, reaching a settlement often requires the assistance of a lawyer or professional negotiator.

How Long Does It Take to Get Garnished Wages Back?

The timeframe for releasing garnished wages depends on the type of debt and how quickly the issue is resolved. In cases of IRS wage garnishment, once a payment plan, hardship or offer in compromise is approved, wage deductions typically stop within one to two pay periods.

However, it can take several weeks for employers to process the change and return to full paychecks which is why we fax the release to the payroll contact for immediate release. For erroneous garnishments or those stopped through legal challenges, refunds may take up to 60 days or longer, depending on how quickly the creditor or IRS processes the case.

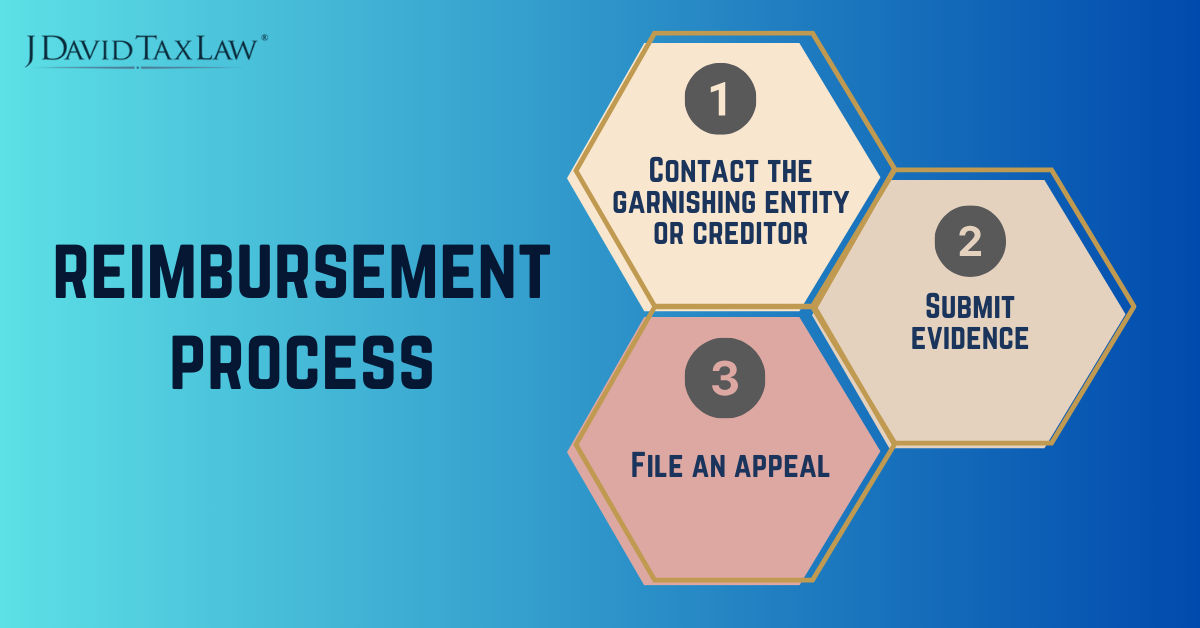

If wages were garnished in error or if the amount withheld exceeded legal limits, the employee may be entitled to a refund. To initiate the reimbursement process, individuals must:

-

Contact the garnishing entity or creditor to formally request a review.

-

Submit evidence of improper garnishment, such as wage statements and garnishment notices.

-

File an appeal with the IRS or court if the garnishment was related to tax or legal debt.

For IRS-related reimbursements, the process can take several weeks to months, depending on the complexity of the case. Non-IRS garnishments may involve coordination between the creditor, employer, and court, which could further delay the refund. Working with a wage garnishment lawyer ensures that all necessary documentation is submitted properly, speeding up the reimbursement process where possible.

Additional Resources and Help

The Wage Earner Protection Program (WEPP) provides financial relief to employees affected by the bankruptcy of their employers. If wages or severance were unpaid due to bankruptcy, employees may apply to this program for reimbursement. This ensures they receive compensation for the work performed before the bankruptcy filing.

A wage garnishment lawyer can offer critical support by identifying errors in garnishment orders, negotiating with creditors or the IRS, and pursuing appeals or exemptions. Legal assistance ensures the garnishment process is fair and protects employee rights.

Lawyers also provide valuable guidance on options such as bankruptcy or hardship exemptions, making it easier to manage or eliminate garnishments.

Conclusion

Wage garnishment can have a significant impact on financial stability, making it crucial to understand how the process works and what options are available to address it. Legal assistance from a wage garnishment lawyer can make a difference, ensuring that garnishments are handled correctly and helping you explore all available relief strategies.

If you’re facing wage garnishment, it’s important to take action early to minimize financial strain. Contact J. David Tax Law wage garnishment attorneys at (888) 342-9436 to resolve your debt issues, stop further garnishments, and regain financial control.