When the IRS comes after unpaid taxes, the situation can quickly escalate from simple notices to more severe actions like wage garnishment or the freezing of your bank account. This process, known as an IRS levy, can have an immediate and profound impact on your financial stability. At J. David Tax Law, we understand the gravity of an IRS levy and the anxiety it can cause. This guide explains the essentials of tax levies, tax liens, and how they can affect your finances—and most importantly, how we can help protect your assets.

Tax Levy Meaning: What Is A Tax Levy?

A tax levy is a legal seizure of your property to settle unpaid tax debts. It differs from a federal tax lien, which is simply a legal claim against your property. A tax levy, however, is an active collection method where the IRS or state tax authorities forcibly take control of your assets. The IRS can levy your:

Wages (wage levy)

Bank accounts

Social Security benefits

Real estate

Vehicles

Retirement accounts

Other personal property

If you’ve ever asked, “What is a tax levy?” or “Why is there a tax levy on my paycheck?”, the answer is straightforward: it means that you failed to pay your taxes after receiving multiple notices from the IRS or state tax agency. Once a levy is initiated, it’s essential to take action quickly before your financial situation worsens.

Want to know how we manage penalties like Failure-to-File, Failure-to-Pay, and Failure-to-Deposit? Call us at (888) 342-9436 for a free consultation today!

Irs Levy Vs. Federal Tax Lien: Understanding The Difference

It’s important to distinguish between an IRS levy and a federal tax lien. A federal tax lien is a legal claim against your property when you owe back taxes. It can damage your credit and prevent you from selling property until the lien is satisfied. However, a tax lien does not involve the immediate seizure of assets.

An IRS levy, on the other hand, is much more aggressive. The IRS will seize your property or money to satisfy the debt. This can include garnishing your wages, freezing your bank accounts, or even seizing your assets.

Understanding the distinction between these two terms is key to knowing how they might affect you.

How Does An Irs Levy Affect You?

An IRS levy can disrupt every aspect of your financial life. Once the IRS decides to levy taxes, the following scenarios may occur:

1. Wage Levy (Garnishment)

A wage levy allows the IRS to take a portion of your paycheck directly from your employer. Unlike a one-time bank levy, wage levies continue until the debt is fully repaid. This can reduce your take-home pay significantly, leaving you with just enough for basic living expenses—or sometimes even less.

2. Bank Levy

An IRS levy on your bank account can freeze your funds for 21 days. During this period, you won’t be able to access your account, and if the tax debt is not resolved by the end of that period, the funds will be transferred to the IRS. Worse, the IRS can issue multiple bank levies if the debt remains unpaid.

3. Property Seizure

In extreme cases, the IRS can seize your property, including homes, vehicles, and other valuable assets. While this is less common than wage or bank levies, it remains a serious threat if other collection efforts fail.

4. Social Security Levy

The IRS can also levy up to 15% of your Social Security benefits, reducing the income you rely on during retirement. This can lead to substantial financial hardship, particularly for those on fixed incomes.

Facing a wage levy or bank account freeze? Let our experienced attorneys help you. Call us at (888) 342-9436 for a free consultation.

Common Irs Levies: What You Need To Know

1. IRS Wage Levy

An IRS wage levy is ongoing, which means the IRS will continue to take a portion of your paycheck until the tax debt is paid off or the levy is released. This can drastically reduce your income, making it difficult to cover basic living expenses like rent, utilities, and groceries.

2. IRS Bank Levy

A bank levy is a one-time seizure of your funds. After freezing your bank account for 21 days, the IRS takes the money to satisfy your debt. This can lead to bounced checks, additional bank fees, and severe financial disruption.

3. State Tax Levy

Like the IRS, state tax authorities also have the power to impose state tax levies on wages, bank accounts, or other assets. Procedures vary by state, but the financial impact can be just as devastating as an IRS levy.

What Does “Levy Taxes” Mean?

In general, to levy a tax means to impose or collect taxes. In the context of an IRS levy, it refers to forcibly collecting taxes from your property or income. The IRS uses this method as one of its most effective enforcement tools when other collection methods fail.

Why Is There A Tax Levy On My Paycheck?

If the IRS has placed a tax levy on your paycheck, it’s because you’ve failed to pay your taxes after multiple notices. Typically, the IRS sends the following notices before initiating a levy:

Notice and Demand for Payment (a bill)

Final Notice of Intent to Levy

Notice of Your Right to a Hearing

Failing to respond to these notices in a timely manner allows the IRS to take drastic measures, such as levying your wages or bank accounts.

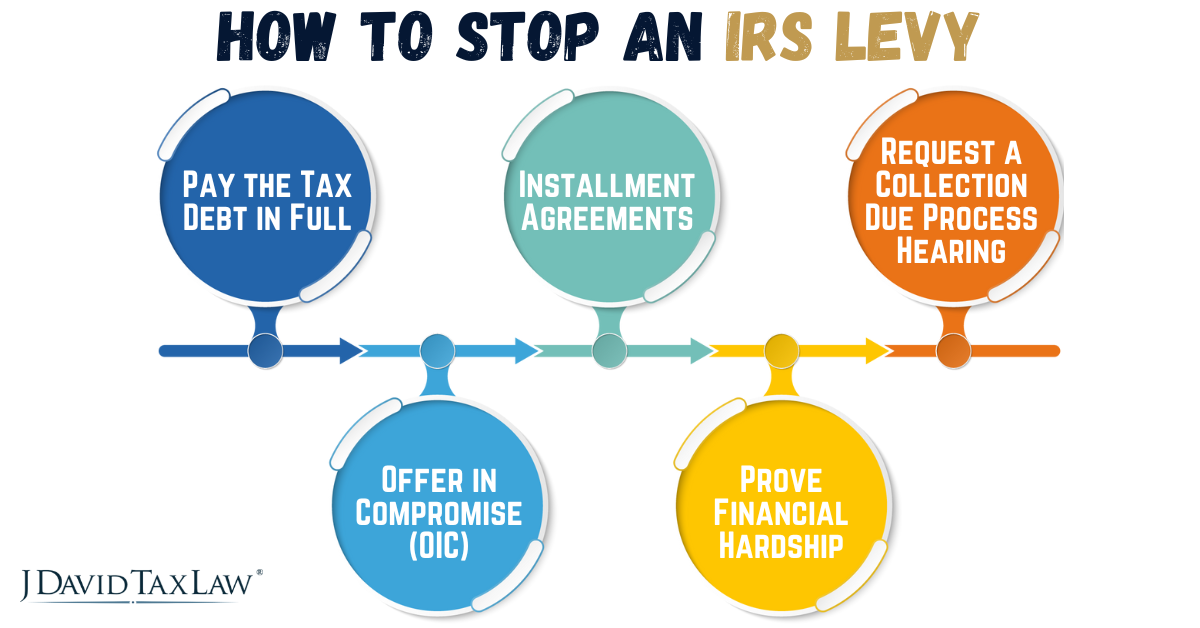

How To Stop An Irs Levy

Stopping an IRS levy requires immediate action. At J. David Tax Law, we specialize in negotiating with the IRS and can help you with the following solutions:

1. Pay the Tax Debt in Full

While this may seem like an obvious solution, many people simply cannot afford to pay their tax debt in a lump sum. However, if you can pay it off, we as tax lien lawyers can expedite the process and get the levy lifted, ensuring the IRS releases the levy quickly.

2. Installment Agreements

If paying the full amount isn’t feasible, as levy tax attorneys, we can negotiate an Installment Agreement with the IRS. This allows you to make manageable monthly payments until the debt is paid off. Once the agreement is in place, the IRS will lift the levy.

3. Offer in Compromise (OIC)

An Offer in Compromise allows you to settle your tax debt for less than you owe. While only a small percentage of OIC applications are approved, we, as levy tax professionals, can help prepare and present a strong case for why your circumstances justify a reduced settlement.

4. Prove Financial Hardship

If the levy causes undue financial hardship, we, as a team of tax lien experts, can demonstrate to the IRS that the levy should be released. This requires detailed documentation of your income, expenses, and liabilities.

5. Request a Collection Due Process Hearing

If you’ve received a Final Notice of Intent to Levy, we, as your representatives, can request a Collection Due Process (CDP) hearing to challenge the levy or propose alternative solutions. This must be done within 30 days of receiving the notice, so timely action is essential.

Need help lifting an IRS levy? Contact J. David Tax Law at (888) 342-9436 for a free consultation. Our firm has over four decades of collective tax debt resolution experience, guaranteeing you the best chance of financial freedom.