As of the latest figures from the U.S. Internal Revenue Service, collected $104.1 billion in unpaid taxes, penalties, and interest by 2022. Despite the risks of harsh penalties, asset seizures, and potential jail time, millions of individuals still find themselves unable to keep up with their tax obligations.

Falling behind on taxes can feel stressed, and the fear of wage garnishments, frozen bank accounts, or relentless IRS letters can keep anyone up at night. But if you genuinely can’t afford to pay right now, the IRS Currently Not Collectible (CNC) status might just be the relief you need.

In this guide, we’ll walk you through everything you need to know about irs uncollectible status, how to qualify, how to apply, and what happens once you’re approved. If tax debt is hanging over your head, understanding CNC status could be your first step toward regaining control.

What is CNC Status?

CNC status means Currently Not Collectible Status. In simple terms, it’s the IRS recognizing your financial hardship and hitting “pause” on their collection efforts. They won’t chase you for payments until your situation improves, giving you a bit of breathing room. If you qualify for Currently Not Collectible Status, the IRS won’t garnish your wages, levy your bank account, or send collection notices while you’re in this status, which usually lasts between six months to two years.

But keep in mind IRS CNC status doesn’t forgive your debt. Interest and penalties will still accumulate, meaning the longer you’re in IRS non collectible status, the more your debt could grow. However, it offers relief from the pressure of immediate payments, giving you time to focus on essentials like rent, food, and other necessary expenses.

The IRS periodically reviews your financial situation to see if anything has changed. If they find that you’re in a better position to pay, they might lift your currently not collectible status and start collection efforts again. Applying for CNC status means showing the IRS that paying your tax debt would cause financial hardship, and this typically requires you to provide detailed financial information, such as your income, expenses, and assets.

Feeling the financial pressure? CNC status could be your lifeline. It can help ease the pressure while you get back on your feet. Talk to a tax expert today.

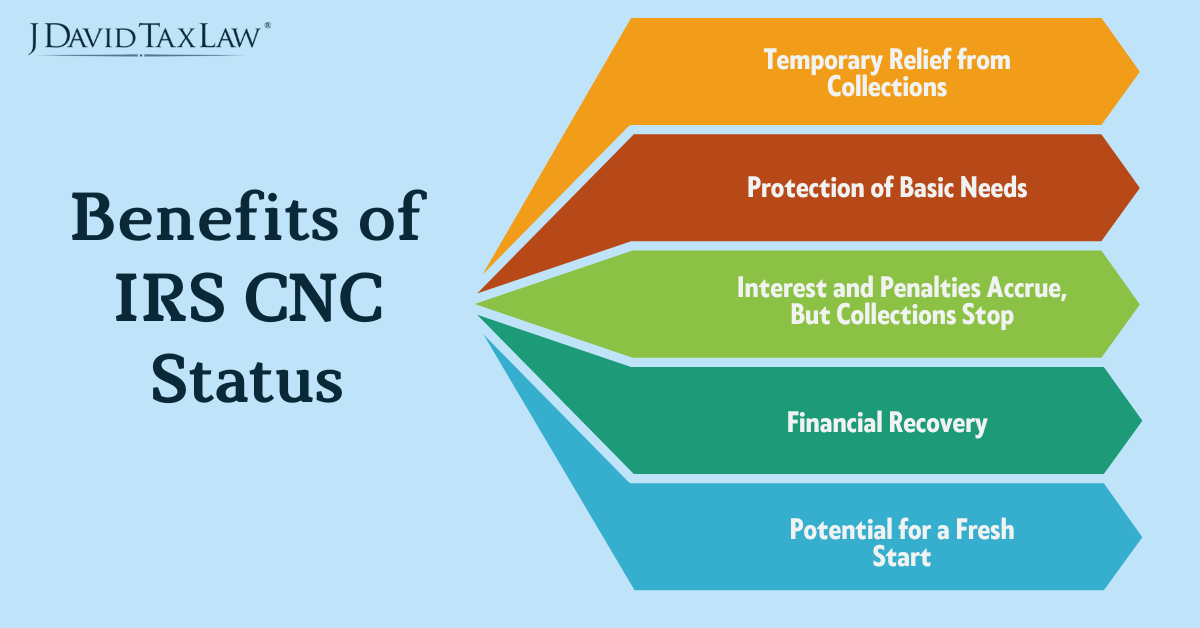

Benefits of IRS CNC Status

Applying for Currently Not Collectible (CNC) status can provide several significant advantages if you’re struggling with tax debt. Here’s a closer look at the benefits you can expect:

Temporary Relief from Collections

One of the most immediate benefits of CNC status is the halt of IRS collection actions. This means you won’t face wage garnishments, bank levies, or collection calls while your status is active. For those in this situation, CNC status can offer breathing room to focus on stabilizing their financial situation without the constant pressure of IRS collections.

Did you know J David can help remove wage garnishment in less than 48 hours? Here’s how

Protection of Basic Needs

CNC status allows you to prioritize your essential living expenses. When you’re approved for CNC, the IRS acknowledges that paying your tax debt would lead to financial hardship. This means you can focus on meeting your basic needs, such as housing, food, and healthcare. With CNC status, you can alleviate some of that stress, knowing that you can keep your home and provide for your family.

Interest and Penalties Accrue, But Collections Stop

While it’s true that interest and penalties continue to accumulate on your tax debt while in CNC status, the critical benefit is that you won’t be subject to aggressive collection tactics. For example, the IRS charged an average interest rate of 3% on unpaid taxes in 2022 during the first quarter. While this means your total debt could grow, it’s often more manageable to focus on your current financial health rather than dealing with immediate collection threats.

Financial Recovery

CNC status can provide a valuable opportunity to get back on your feet financially. With the IRS temporarily pausing collection efforts, you can use this time to create a budget, increase your income, or explore new employment opportunities. Many individuals find that being in CNC status allows them to stabilize their finances and eventually work towards resolving their tax debt.

Potential for a Fresh Start

If your financial situation improves while in CNC status, you can later explore options like an Offer in Compromise or payment plans. The IRS allows you to reapply for CNC status if you find yourself struggling again. This flexibility means that you’re not locked into one solution.

To learn more visit https://www.jdavidtaxlaw.com/offer-in-compromise/

How to Apply for IRS Non-Collectible Status

Here’s a simple guide on how to file currently not collectible with the IRS:

Steps to Apply for CNC Status:

Complete the Necessary Forms: You’ll likely need to fill out IRS Form 433-F (Collection Information Statement) or Form 433-A (for self-employed or individuals with more complex finances). These forms require you to provide details about your income, expenses, assets, and debts.

Provide Documentation: Be prepared to back up your application with proof. This includes:

Recent pay stubs or proof of income

Bank statements

Rent/mortgage payments

Utility bills

Medical bills, if applicable These documents will help the IRS determine if you truly can’t afford to pay your tax debt right now.

Show Financial Hardship: The key to qualifying for CNC is proving that paying your tax debt would create financial hardship, making it impossible to cover necessary living expenses. Your forms and supporting documents should clearly demonstrate this.

Wait for IRS Review: After you submit your paperwork, the IRS will review your financial situation. This can take a few weeks. If approved, the IRS will pause its collection efforts.

Don’t let the IRS get the best of you. To take to an expert tax attorney visit https://www.jdavidtaxlaw.com/contact-us/ to protect your financial future.

If you’re considering applying for IRS Currently Not Collectible (CNC) status, it’s essential to understand the requirements the IRS has in place.

Demonstrated Financial Hardship: The IRS needs to see that paying your tax debt would create a financial burden. This means your monthly income must be lower than your necessary living expenses. You must show that you can’t meet your basic needs, such as housing, food, and healthcare if you were to pay your taxes.

Detailed Financial Information: When you apply, you’ll need to provide comprehensive information about your finances. This includes:

Income: Document all sources of income, including salaries, Social Security, disability, or any other funds.

Expenses: List all monthly expenses like rent/mortgage, utilities, groceries, transportation, and any medical costs.

Assets: Be transparent about any assets you own, such as property, vehicles, or savings accounts. If your assets are minimal or encumbered by debt, it may strengthen your case.

No Recent Tax Payments: To qualify for CNC status, you shouldn’t have made any recent payments towards your tax debt. The IRS wants to ensure that you truly cannot afford to pay anything right now.

Compliance with Tax Filing: You must be compliant with your tax filing obligations. This means you should have filed all required tax returns for the past few years. If you haven’t, the IRS may require you to file those before considering your CNC application.

Regular Review by the IRS: Once granted CNC status, the IRS will periodically review your financial situation—typically every one to two years. They’ll want to see if your circumstances have changed, so it’s crucial to stay on top of your financial situation.

How the IRS Reviews Your CNC Status Application

The IRS typically conducts reviews at least once a year to assess your eligibility for CNC status. During this review, they examine your financial situation to determine whether you still qualify based on your current income, expenses, and overall financial health.

For that, you may need to provide updated financial information, including documentation of your income through recent pay stubs or tax returns. They also will want to see detailed records of your monthly expenses, such as rent, utilities, groceries, and healthcare costs. The IRS will also look at any assets you own, like properties or savings accounts, to evaluate whether you could liquidate them to pay off your tax debt.

Can IRS CNC Affect Your Credit Score?

Currently not collectible status does not directly affect your credit score, as the IRS does not report debts to credit bureaus. However, if your tax debt exceeds $10,000, the IRS may issue a Notice of Federal Tax Lien.

This public notice can harm your credit by appearing on your report, making it harder to secure loans or credit. Additionally, while CNC halts active collection, interest and penalties continue, and the IRS can seize future refunds to reduce your debt until the statute of limitations expires.

Conclusion

To sum up, the IRS “Currently Not Collectible” (CNC) status can be a critical financial relief for individuals facing significant financial hardships. While it doesn’t eliminate your tax debt, it temporarily halts IRS collection efforts, offering you time to recover without the constant pressure of payments, wage garnishments, or account freezes.

CNC status, however, comes with ongoing interest and penalties, so it’s essential to explore long-term solutions once your financial situation stabilizes. It’s a tool to help you regain control and plan for future tax resolution options.